Bad Credit? 3 Ways Small Business Owners Can Still Get Funded in 2026

The traditional lending world has a very long memory. If you had a financial setback in 2022 or 2024, most big banks will still treat your application as a “non-starter” in 2026. They are tethered to the FICO score—a single three-digit number that rarely tells the whole story of a resilient, revenue-generating business.

But the 2026 capital market is no longer a monopoly. While banks have spent the last year tightening their belts and raising their credit requirements, a new era of performance-based lending has gone mainstream.

If you have strong sales but a “sub-prime” credit score, here are the three most effective ways to secure funding today.

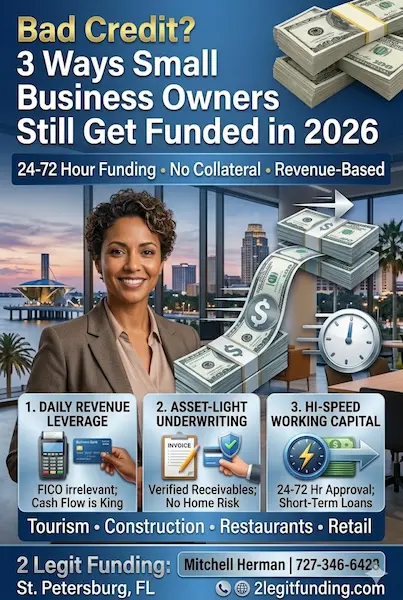

1. Leverage Your Daily Revenue (Revenue-Based Financing)

In 2026, the most successful “bad credit” funding model is Revenue-Based Financing (RBF). This is not a traditional loan with a fixed monthly payment; it is an advance against your future sales.

How it works: Instead of looking at your personal credit history, funders look at your business bank statements from the last 3-6 months. They want to see consistent daily or weekly deposits.

- The “Bad Credit” Benefit: Your FICO score takes a backseat to your cash flow. If your business is moving product or booking services daily, you are fundable.

- The Flexibility: Payments are usually a fixed percentage of your sales. If you have a slow week, the amount you remit drops automatically, protecting your remaining working capital.

2. Utilize “Asset-Light” Underwriting

Traditional lenders want “hard” collateral: real estate, heavy machinery, or a personal guarantee backed by your home. In 2026, many alternative funders have shifted to “asset-light” models. They treat your accounts receivable or your consistent credit card volume as the primary security.

If you run a service business, a restaurant, or a retail shop, your “asset” is your customer base. Alternative funders use AI-driven underwriting to analyze your sales patterns and project your future stability. This allows them to say “yes” to business owners who don’t have a million dollars in equipment to pledge but do have a loyal, paying clientele.

3. High-Speed Working Capital Loans

Speed is often a proxy for trust in the 2026 lending environment. Many fintech platforms now offer short-term working capital loans that can be approved and funded in 24 to 72 hours.

Because these loans have shorter durations (typically 6 to 18 months), the lender’s risk is lower than a 10-year bank loan. This lower risk profile allows them to be much more lenient with credit scores. They aren’t betting on where you’ll be in a decade; they are betting on the fact that your business will continue to perform over the next year.

The Truth About Funding in 2026

Your credit score is a reflection of your past, but your revenue is a reflection of your present. In the modern economy, your ability to generate cash is a far more accurate measure of “creditworthiness” than a score calculated by a bureau that has never stepped foot in your office.

At 2 Legit Funding, we specialize in the “Now.” We don’t care about the “Bank Runaround” or the mistakes of the past. If your business is making money today, we can help you get the capital you need to make more tomorrow.

Don’t let a number hold you back. Let your revenue speak for itself.

Mitchell Herman

2 Legit Funding

727-346-6423

#BadCreditBusinessLoans #SmallBusinessFunding2026 #RevenueBasedFinancing #WorkingCapital #NoCollateralLoans #BusinessGrowth #2LegitFunding #AlternativeFinance